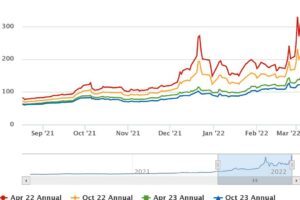

In the last 2 weeks where President Putin has been described as going ‘full tonto’ and forward energy prices have risen by 40%, leading philanthropic energy trading experts Box Power ask how does this affect the business sector and how should it act?

Prices had already risen 145% since last May up to the invasion. Box Power, the energy trading experts to major energy users, who accurately predicted and warned about the risk of the current crisis and its repercussions afterwards, gives stark warnings as they see more upward risk of pain to come.

What is happening? In the year where it was financially prudent to hope for the best but plan for the worst, then anyone on the wrong side of the invasion will now have costly burnt fingers. With the EU turning up the heat on Russia with financial sanctions, more recently excluding Russia from the banking process SWIFT and a possible retaliation by Russia by turning down the gas to the EU, many were already facing 90% energy cost rises up to these events. For many only now is the realisation, that the huge extra cost impact by missing out on the crucial right advice will undoubtedly cause extra financial stress on top of their many other inflationary pressures.

How did Box Power advise its own clients? Back in early January Box Power had flagged within their 2022 market prediction that they saw the President Putin/Ukraine issue as their single biggest material concern of the year and that any 2022 risk exposure should be based on this. Clients were warned therefore to start any tender process urgently, so they would have their ‘proverbial ducks lined up’ and be ready to implement the best market options as instantly needed. Box Power had flagged concerns that the rhetoric and action between Russia and the West would get to the point where the Nordstream2 pipeline would be cancelled, which would spike prices based on future supply/demand worries.

With the Nodstream1 often already reversing direction during January, it became clear that any risk to Nord2 would have an impact on Nord1 and other pipelines feeding into the EU. As the situation evolved in late January, Box Power highlighted the need to start taking large amounts of risk off the table by securing new long-term deals. Box Power viewed February as a misleadingly quiet month in the crisis because of the Winter Olympics and issued more recommendations right up to last Tuesday morning before prices spiked on the inevitable news that Nord2 was cancelled.

Box Power’s view was that in the event that the situation escalated, President Biden’s attempt to reassure the EU that it won’t run out of gas could mean that prices rose even higher to compensate. After all there are only a certain number of available LNG tankers and simply diverting the LNG gas from Asia to the EU would just cause Asia to simply bid higher to ensure they remain fully supplied and we would pay the same spot price.

How could this impact supplier choice? Many operators will be aware that energy suppliers were already sensitive to credit risk from many business sectors, so the current unstable situation will no doubt encourage a higher number of energy suppliers to include higher risk premiums into their prices.

What is the Box Power advice today for CHP readers? Readers may recall our warning last May when we flagged gas supply replenishment as a key concern for this current winter, which then saw prices spike higher afterwards. With warnings to the EU to expect to see 100%+ gas price increases, given Russia is in complete control and has logical reason to retaliate with this weekend’s SWIFT exclusion pressures, we see material risk to a reduction in supply into the EU that would panic the gas markets. The markets would see risk that the EU (and UK) would face an even worse resupply issue with gas reductions next winter.

Box Power’s advice today is – quickly switch to the right advice; reconsider your appetite of further upward risk; as soon as markets allow be ready to act quickly; but don’t be surprised if many suppliers are reluctant to price, include much higher risk premiums, require security deposits or decline altogether.